Statistical Tables | | Right Down The Hall, For Now

| Trends at a Glance | |||

| (Single-family Homes) | |||

| Apr 26 | Mar 26 | Apr 25 | |

| Home Sales: | 230 | 181 | 214 |

| Median Price: | $1,560,000 | $1,598,000 | $1,750,000 |

| Average Price: | $2,343,538 | $2,273,689 | $2,163,736 |

| SP/LP: | 99.4% | 100.6% | 111.0% |

| Days on Market: | 16 | 18 | 22 |

| (Lofts/Townhomes/TIC) | |||

| Apr 26 | Mar 26 | Apr 25 | |

| Condo Sales: | 262 | 246 | 218 |

| Median Price: | $1,199,500 | $1,200,000 | $1,099,000 |

| Average Price: | $1,426,528 | $1,448,437 | $1,553,715 |

| SP/LP: | 99.4% | 99.2% | 94.6% |

| Days on Market: | 30 | 33 | 48 |

The median sales price for single-family, re-sale homes was down 10.9%

year-over-year.

The average sales price for single-family, re-sale homes was up 3.1%

month-over-month. Year-over-year, it was up 8.3%.

Sales of single-family, re-sale homes rose 7.5% year-over-year. There were 230

homes sold in San Francisco last month. The average since 2000 is 214.

The median sales price for

condos/lofts

was up 9.1% year-over-year.

The average sales price was down 8.2% year-over-year.

Sales of

condos/lofts

rose 20.2% year-over-year. There were 262

condos/lofts

sold last month. The average since 2000 is 230.

The sales price to list price ratio, or what buyers are paying over what sellers

are asking, fell from 100.6% to 99.4% for homes. The ratio for condos/townhomes

rose from 99.2% to 99.4%.

Average days on market, or the time from when a property is listed to when it

goes into contract, was 16 for homes and 30 for condos/lofts.

Sales momentum…

for homes rose from +0.7 to +1.3. Sales momentum for condos/lofts was up 0.4 of

a point to +11.8.

Pricing momentum…

for single-family homes fell 0.9 of a point to -6.4. Pricing momentum

for condos/lofts was up 0.6 of a point to +0.3.

Our momentum statistics are based on 12-month moving averages to eliminate

monthly and seasonal variations.

If you are planning on selling your property, call me for a free comparative

market analysis.

momentum by using a 12-month moving average to eliminate seasonality. By comparing this year's 12-month moving average to last year's, we get a percentage showing market momentum.

the blue area shows momentum for home sales while the red line shows momentum for pending sales of single-family, re-sale homes. The purple line shows momentum for the average price.

As you can see, pricing momentum has an inverse relationship to sales momentum.

The graph below shows the median and average prices plus unit sales for homes.

Remember, the real estate market is a matter of neighborhoods and houses. No two are the same. For complete information on a particular neighborhood or property, call me.

P.S. The FHA requires all condo projects to be re-certified before they will make a loan. To find out if the condo project you're interested in is eligible, go here: https://entp.hud.gov/idapp/html/condlook.cfm.

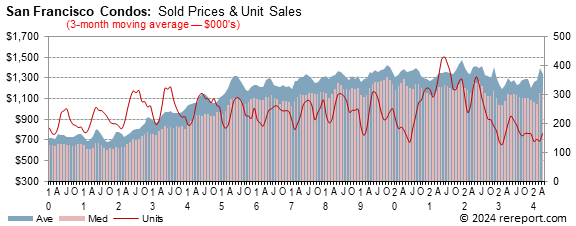

The graph below shows the median and average prices plus unit sales for condos/lofts.

The real estate market is very hard to generalize. It is a market made up of many micro markets. For complete information on a particular neighborhood or property, call me.

If I can help you devise a strategy, call or click the buying or selling link in the menu to the left.

Complete monthly sales statistics for San Francisco are below. Monthly graphs are available for each area in the city.

| April Sales Statistics | |||||||||||

| (Single-family Homes) | |||||||||||

| Prices | Unit | Yearly Change | Monthly Change | ||||||||

| Median | Average | Sales | DOM | SP/LP | Median | Average | Sales | Median | Average | Sales | |

| San Francisco | $1,560,000 | $2,343,538 | 230 | 16 | 99.4% | -10.9% | 8.3% | 7.5% | -2.4% | 3.1% | 27.1% |

| D1: Northwest | $3,015,000 | $4,125,000 | 19 | 45 | 125.8% | 30.2% | 53.5% | 0.0% | 30.0% | 46.0% | 26.7% |

| D2: Central West | $2,003,888 | $2,247,938 | 39 | 18 | 128.8% | 18.6% | 28.1% | -25.0% | 3.8% | 1.0% | -4.9% |

| D3: Southwest | $1,700,000 | $1,928,089 | 10 | 23 | 129.9% | 22.7% | 30.3% | -44.4% | 3.7% | 4.8% | 25.0% |

| D4: Twin Peaks | $2,417,500 | $2,550,321 | 28 | 11 | 124.3% | 24.0% | 10.2% | 7.7% | -0.3% | -3.7% | -15.2% |

| D5: Central | $3,400,000 | $3,520,340 | 34 | 14 | 123.8% | 19.0% | 24.7% | 9.7% | 20.8% | -5.1% | 70.0% |

| D6: Central North | $1,992,500 | $2,417,500 | 4 | 10 | 114.0% | -48.1% | -37.0% | 100.0% | n/a | n/a | n/a |

| D7: North | $6,880,000 | $9,102,273 | 11 | 27 | 112.2% | 60.0% | 72.8% | 10.0% | -7.7% | 10.5% | -8.3% |

| D8: Northeast | $6,600,000 | $11,633,333 | 3 | 9 | 107.4% | 48.3% | 161.4% | 200.0% | n/a | n/a | n/a |

| D9: Central East | $2,025,000 | $2,207,833 | 30 | 17 | 123.3% | 6.6% | 10.9% | 30.4% | 28.0% | 13.6% | 25.0% |

| D10: Southeast | $1,264,000 | $1,279,613 | 52 | 18 | 119.3% | 19.0% | 14.3% | 62.5% | 2.8% | 2.1% | 85.7% |

| April Sales Statistics | |||||||||||

| (Condos/TICs/Co-ops/Lofts) | |||||||||||

| Prices | Unit | Yearly Change | Monthly Change | ||||||||

| Median | Average | Sales | DOM | SP/LP | Median | Average | Sales | Median | Average | Sales | |

| San Francisco | $1,199,500 | $1,426,528 | 262 | 30 | 99.4% | 9.1% | -8.2% | 20.2% | 0.0% | -1.5% | 6.5% |

| D1: Northwest | $1,605,000 | $1,739,493 | 16 | 31 | 115.4% | 46.9% | 55.9% | 14.3% | -13.6% | 0.8% | 128.6% |

| D2: Central West | $1,010,000 | $1,170,474 | 5 | 40 | 105.3% | -23.0% | -18.2% | 25.0% | n/a | n/a | n/a |

| D3: Southwest | $715,000 | $898,167 | 3 | 39 | 100.8% | -22.9% | -3.1% | 50.0% | 13.0% | 42.0% | 50.0% |

| D4: Twin Peaks | $950,000 | $951,375 | 8 | 40 | 105.4% | -9.1% | -9.0% | 300.0% | 21.0% | 20.3% | 60.0% |

| D5: Central | $1,470,000 | $1,526,357 | 35 | 26 | 118.3% | 10.5% | 5.1% | 2.9% | -16.0% | -18.5% | 0.0% |

| D6: Central North | $1,615,000 | $1,550,791 | 21 | 19 | 118.8% | 56.0% | 40.4% | 61.5% | 94.7% | 49.8% | -12.5% |

| D7: North | $1,591,250 | $2,257,034 | 37 | 21 | 109.6% | -16.3% | -28.2% | 5.7% | -12.3% | -2.5% | -2.6% |

| D8: Northeast | $1,225,000 | $1,584,447 | 49 | 25 | 105.1% | 18.9% | 19.9% | 36.1% | 6.5% | 25.3% | 0.0% |

| D9: Central East | $1,299,000 | $1,390,060 | 75 | 41 | 104.0% | 32.6% | 10.1% | 4.2% | 8.3% | -10.4% | 1.4% |

| D10: Southeast | $810,000 | $789,257 | 7 | 43 | 102.8% | 31.1% | 18.9% | 16.7% | -15.6% | -15.4% | 133.3% |

May 1, 2026 --

Sometime in the middle of next month, it's going to be a new day for the Fed, as

Kevin Warsh will become Chair of the Federal Reserve, and will take the helm of

the Federal Open Marked Committee, the body charged with evaluating economic

conditions and setting the course for monetary policy. While such a changeover

is fairly routine, what's not routine is for the former Chair of the committee

to remain with the Fed. This week, we learned that current Fed Chair Jerome

Powell intends to do just that, returning to the Governor's seat he held before

being elevated to lead the Fed back in 2018.

Some eight years ago, Mr. Powell succeeded then-Chair Janet Yellen, someone he

had worked with for six years before she departed. At his press conference, he

noted that "we were sitting down the hall from each other," and the transition

at that time saw him elevated as she exited. In Chair Powell's words, the

upcoming process will be 'a very different thing" than what took place back

then. Mr. Powell will move back to a position right down the hall again, and

will remain there "for a period of time to be determined." While he remains, Mr.

Powell pledged to be a "low profile" Governor.

Aside from the transition drama and what it may mean for the Fed going forward,

the FOMC voted this week to hold policy rates steady again, leaving the federal

funds rate with a range of 3.5% to 3.75%. All but one voting member agreed with

the decision to remain pat; Mr. Miran again agitated for lower rates, as he has

done since joining the board last September. While his was the only dissent in

terms of policy action, three other FOMC members didn't agree with the implicit

message in the meeting-closing statement that the next move by the FOMC would

likely be a cut in interest rates. Beth M. Hammack, Neel Kashkari and Lorie K.

Logan all preferred a more balanced statement, suggesting that policy rates

might have an equal chance of remaining the same or even being lifted in the

foreseeable future.

The housing market may not be on great footing -- Mr. Powell characterized it as

having remained "weak" -- but there was a sizable upturn in housing starts in

March anyway. A 10.8% increase compared to February lifted overall housing

starts to a 1.502 million annualized pace, Single-family starts rose to a 1.032

million rate, the fastest pace of construction initiation for one-family

dwellings in more than a year. Multi-family construction also flared higher,

moving up from 415K annual units in February to 470,000 for March. However,

while the present looks great, the future is considerably less bright. Permits

for future building activity declined by 10.8%, with new permits for

single-family homes falling 3.8% to 895,000 annualized units expected to be

started, while multi-unit building permits declined 21.5%.

Applications for mortgage credit slid by 1.6% in the week of April 24. The

Mortgage Bankers Association reported that requests for funds to purchase homes

managed to increase by 1.2% for the week, but those to refinance existing

mortgages dropped off by 4.4%. Mortgage rates have been fairly well-behaved

given inflation concerns and upward pressure on longer-term interest rates, but

they aren't currently at a place that supports a faster pace of homebuying or

one that increases opportunities for homeowners to refinance. As such, sluggish

activity is about all that can be expected.

This page is copyrighted by https://rereport.com. All rights are reserved.